Ready to Finance Your Next CRE Investment? A Gut Check on Your Credit Box Triangulation

Ready to Finance Your Next Real Estate Investment?

A Gut Check on Your Credit Box Triangulation

By John R. Kraus, MBA

Premier Credit Insights & Solutions LLC

Many investors spend months finding the right property. Few spend enough time understanding how lenders evaluate the deal.

Before you submit your next commercial real estate loan request, ask yourself:

Would you approve this deal if you were the bank?

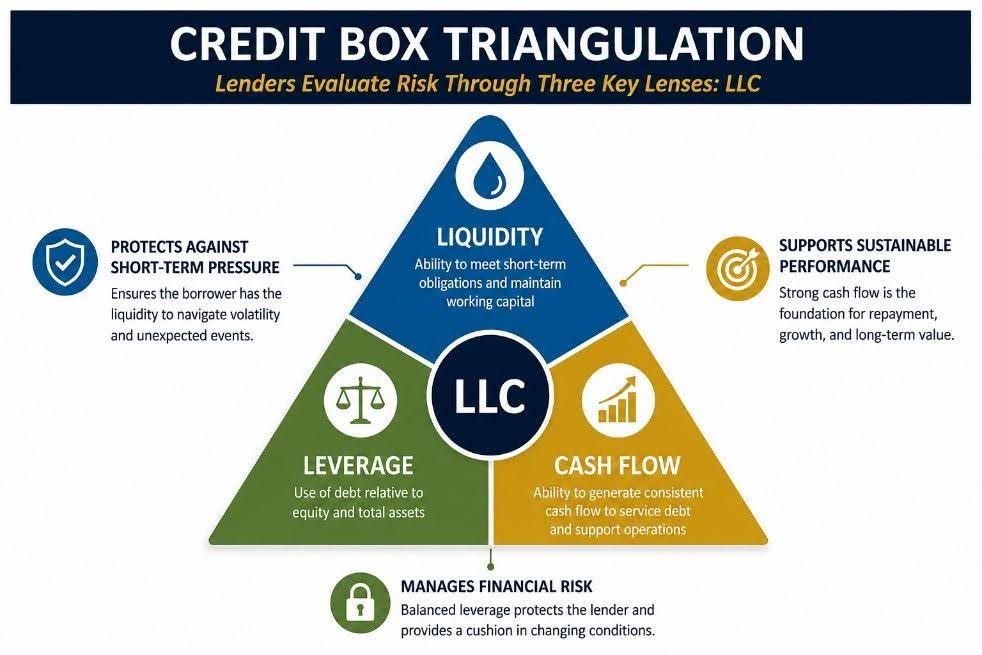

Experienced lenders typically evaluate commercial real estate loans through three primary underwriting lenses:

The Credit Box Triangulation

At its core, every commercial real estate loan request must answer three questions:

Can the property generate enough cash flow to repay the loan?

Is there sufficient equity supporting the transaction?

Does the property's income justify the lender's exposure?

These questions translate into three key underwriting metrics:

Debt Service Coverage Ratio (DSCR)

Loan-to-Value / Loan-to-Cost (LTV/LTC)

Debt Yield

Think of these three measurements as the legs of a stool. When one weakens, the others often need to compensate.

Successful borrowers understand that loan approval rarely depends on a single metric. It depends on how all three work together.

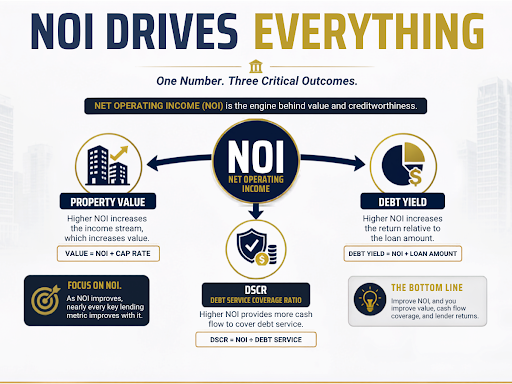

NOI: The Common Denominator

Before discussing each metric, investors should understand the concept that drives virtually every commercial real estate financing decision:

Net Operating Income (NOI)

NOI represents a property's income after operating expenses, but before mortgage payments, taxes, depreciation, and capital expenditures.

Simply stated:

NOI is the engine that drives both commercial real estate value and creditworthiness.

NOI directly impacts all three pillars of the Credit Box Triangulation.

DSCR measures whether NOI is sufficient to cover debt payments.

Debt Yield is calculated directly from NOI:

Debt Yield = NOI ÷ Loan Amount

And because commercial real estate is often valued using the Income Capitalization Approach:

Value = NOI ÷ Cap Rate

a higher NOI generally increases property value as well.

For example:

NOI = $200,000

Market Cap Rate = 6.0%

Estimated Value:

$200,000 ÷ 0.06 = $3.33 million

This is why experienced investors often focus first on increasing NOI. As NOI improves, nearly every important lending metric improves with it.

Pillar #1: Debt Service Coverage Ratio (DSCR)

DSCR measures a property's ability to generate sufficient cash flow to make mortgage payments.

In simple terms:

How many dollars of cash flow are available for every dollar of debt service?

Most lenders prefer minimum DSCR levels between1.20x and 1.35x, depending on property type and risk profile.

A DSCR of 1.25x means the property generates $1.25 of cash flow for every $1.00 of required debt payments.

Strong DSCR provides a cushion against vacancies, unexpected expenses, and changing market conditions.

From a lender's perspective, cash flow remains the primary repayment source.

Pillar #2: Loan-to-Value (LTV) and Loan-to-Cost (LTC)

LTV measures the loan amount relative to a property's appraised value.

LTC measures the loan amount relative to total project cost and is commonly used for construction and redevelopment financing.

Typical lending parameters often range between:

70%-80% LTV for stabilized properties

75%-85% LTC for construction projects

Why does this matter?

Because equity creates protection.

The more capital investors contribute, the greater the cushion against declining property values, lease-up challenges, cost overruns, and other unforeseen risks.

In lender terminology, this is commonly referred to as having"skin in the game."

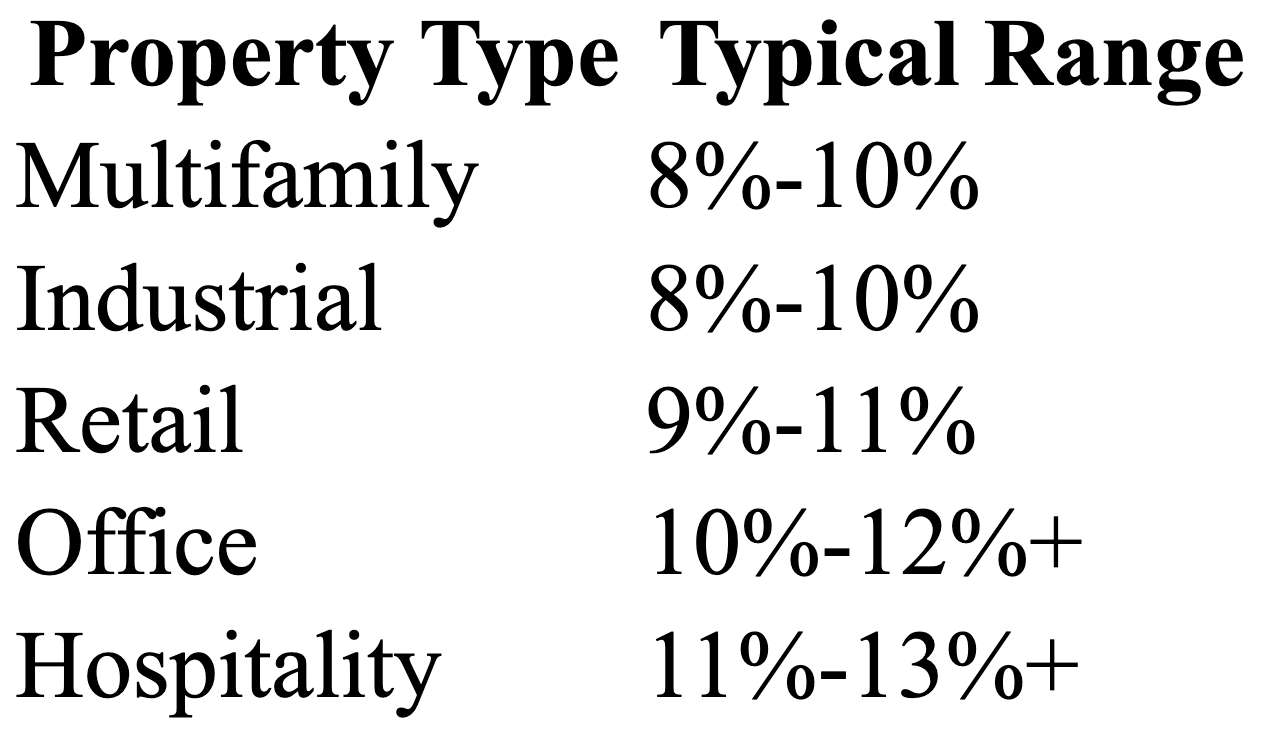

Pillar #3: Debt Yield

Debt Yield has become increasingly important in today's commercial real estate environment.

The formula is simple:

Debt Yield = NOI ÷ Loan Amount

Unlike DSCR, Debt Yield ignores interest rates and amortization schedules. It focuses solely on the relationship between property income and lender exposure.

Typical minimum Debt Yield targets often include:

Think of Debt Yield as a lender's measure of income support for a loan. The more uncertain or volatile a property's cash flow, the more income lenders typically want to see supporting each dollar lent. That is why higher-risk property types generally require higher debt yields than lower-risk property types.

Following recent disruptions in commercial real estate markets, many lenders now place greater emphasis on Debt Yield than ever before.

The Growing Popularity of DSCR Loans

A growing number of investors are exploring financing through non-bank lenders offering DSCR loans.

Unlike traditional bank financing, these lenders focus primarily on the property's ability to support debt service rather than the borrower's overall financial profile.

The appeal is understandable.

Advantages

✓Faster approvals

✓Simplified documentation

✓Reduced emphasis on personal income verification

✓Attractive for investors with multiple properties

✓Flexibility for self-employed borrowers

Potential Drawbacks

✓Higher interest rates

✓Increased fees and closing costs

✓Potentially lower leverage

✓Less flexibility during challenging periods

✓Limited relationship banking benefits

For investors focused on speed, convenience, and transactional execution, DSCR financing can be an effective tool.

However, many borrowers are surprised to discover that traditional banks and credit unions may offer significantly lower borrowing costs, more favorable loan structures, and greater flexibility when a borrower demonstrates strong liquidity, net worth, cash flow, and management experience.

Equally important, community banks and credit unions are relationship-driven institutions. Beyond providing financing, they often serve as trusted advisors, helping investors navigate future acquisitions, refinancing opportunities, treasury management, and long-term capital planning.

While transactional financing can solve an immediate need, many investors ultimately discover that building a long-term banking relationship becomes increasingly valuable as their portfolio grows in size and complexity.

A Final Gut Check

Experienced investors understand that financing is not obtained after a transaction is identified, it is often won or lost during the structuring process.

The strongest borrowers think like lenders long before the loan application is submitted.

Understanding your Credit Box Triangulation before approaching a lender can significantly improve your chances of approval and often result in more favorable financing terms.

About Premier Credit Insights & Solutions LLC

Premier Credit Insights & Solutions helps business owners, real estate investors, developers, and contractors understand how lenders evaluate risk, structure financing requests, and prepare bank-ready loan presentations.

Think Like the Bank Before You Apply.